The Importance of Robust Angel Ecosystems

Earlier this week I gave the keynote address at the Colorado Angel Capital Summit. While the audience was Colorado focused, the overall message I delivered about the angel ecosystem is very relevant to all entrepreneurial communities. I thought I’d share both the presentation and the key thoughts here.

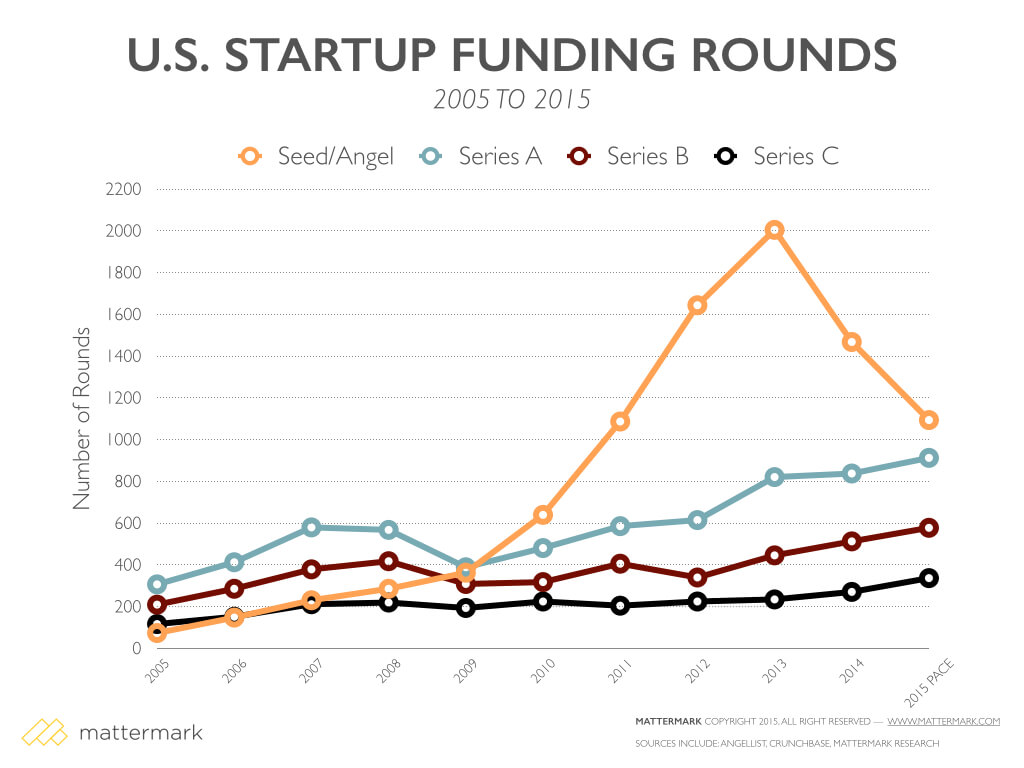

The overall trend around angel investing is a pretty interesting one. I’ve talked about this trend before – specifically the acceleration of angel investing in 2011-2014. I think what we’re really seeing here is market excitement around angel investing leading to a quick surge, followed by (I hope) a more normal and sustained level of activity. The sharp rise in angel activity also coincided with the raise of platforms such as AngelList which more easily allowed investors to find interesting companies and to some extent broadened the geographic reach of angels, extending what had been a more localized activity. If you’ve ever participated in a running or cycling race your heart rate graph probably looked similar – you’re excited at the start of the race and go out a bit strong, only to settle back into the right rhythm. I suspect that’s a bit of what we’re seeing here.

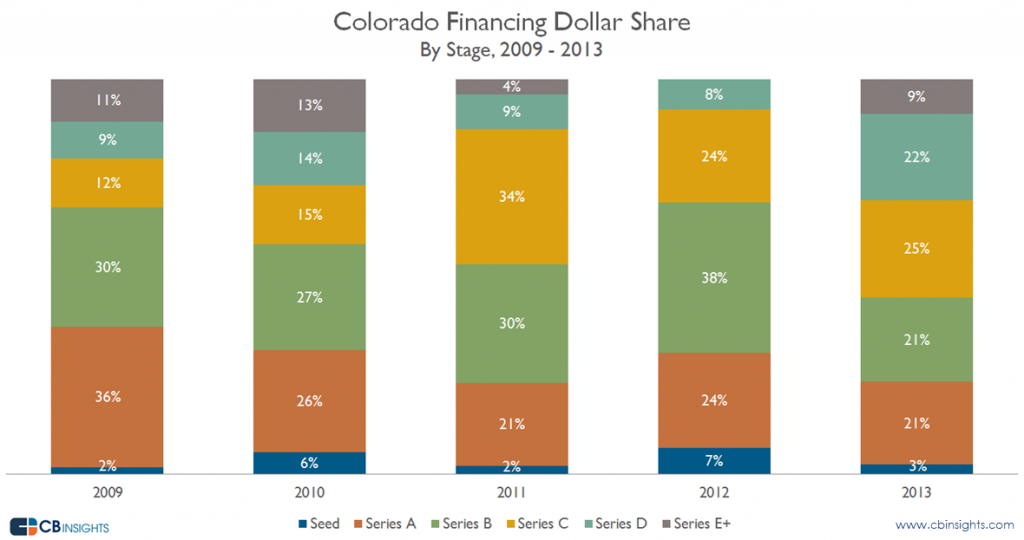

I’ve always felt that a robust angel financing market was important to startup ecosystems and the data on the next two charts really brings that home. These data are specific to Colorado (since my presentation was to a CO audience) but the trend holds true across startup ecosystems. Looking at the dollar share of investing, not surprisingly investing at the Angel/Seed level barely registers, with well less than 10% share (under 5% in a few years).

I’ve always felt that a robust angel financing market was important to startup ecosystems and the data on the next two charts really brings that home. These data are specific to Colorado (since my presentation was to a CO audience) but the trend holds true across startup ecosystems. Looking at the dollar share of investing, not surprisingly investing at the Angel/Seed level barely registers, with well less than 10% share (under 5% in a few years).

{kind=link}

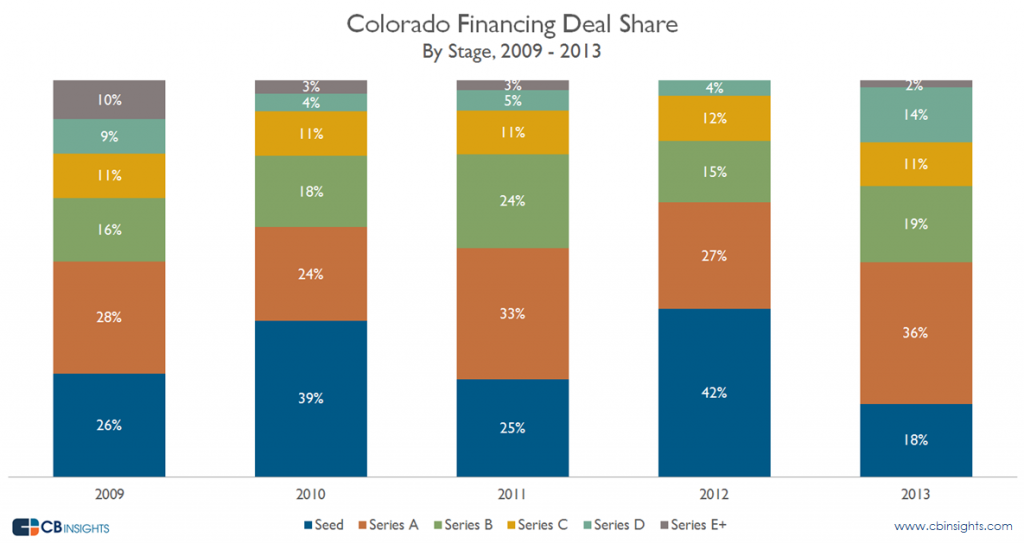

But looking at Seed investing on a deal share basis shows just how impactful this money is to a startup ecosystem – a significant number of companies in any given year raise capital from Angel/Seed investors. Clearly access to capital at this stage has been, and continues to be, critical to the success of the Colorado (and national) startup ecosystem.

While there’s a lot of seed stage investing going on in Colorado and other markets, there are some clear challenges to how many angel investors are approaching the market. I hit these hard in my talk and I’m going to reinforce them here. Angel investors need to do a better job aligning their outcomes with that of the companies in which they invest and the ecosystems they support. Many are approaching the market in ways that are antithetical to successful startup investing. Specifically:

Put Entrepreneurs First. We talk about this a lot at Foundry because it’s the core of our investment philosophy. It’s reflected in how we treat entrepreneurs, how we work with our portfolio companies and the kind of structures we use for our investments. Too many angels don’t embody this and it creates misalignment between them, the companies in which they invest, and between them and later round investors. Even at the angel level terms should be clean, fair and align with management (preference multiples, “$50k for half your company”, etc are neither clean nor fair – to use specific examples that I’ve seen in the market).

Angels are often unorganized and have scattered and burdensome investment processes. Most angel deals happen in syndicates (meaning multiple investors participate), yet many angels are extremely poor at working together with other potential investors. The results are burdensome on a company, result in the duplication and overlap of due diligence and force too much of the syndication work on the company itself. Good angel investors develop a thesis around an investment, bring in the appropriate resources to reach an investment decision, are secure in that opinion without the need for other investors to validate their belief and then work with a company to bring a deal together rather than sit on the sidelines and see what happens. Too many angel investors waste company time, wait for others to validate their decisions and aren’t helpful in getting a round to come together even after they’ve nominally decided to invest.

Successful angel investing requires diversification. I (somewhat) jokingly said during my talk that angel investors should pick an amount of money that they’re willing to light on fire, then divide by at least 10 (better yet 20) to figure out how much they should invest in any given deal. While I know there are some that like to concentrate their bets, the history of angel investing suggests otherwise – there’s such a high mortality rate among early stage companies that a successful angel portfolio needs some level of diversification (baring that, you’re just playing the lottery and hoping to get lucky).

Successful angel ecosystems have active angel mentor networks. With the explosion of accelerators most startup communities around the country and the world are developing very robust mentor networks for companies. Very few of these markets have any even remotely similar at the investor level. That’s a problem, as the same kind of mentoring that takes place between seasoned executives and startups needs to also take place between successful angel investors and new investors. In my view, angel investors are not at all competitive with one another in a market (although many wrongly believe that they are competing for the “best” deals) – they can only make their own investment portfolios stronger by strengthening the overall angel ecosystem in their market.

There’s quite a bit more from the presentation but these are some of the important ideas that I wanted to highlight. The full presentation is embedded below for you to click through if you’re interested. There’s also some interesting data that we haven’t published yet on the 66 companies that ended up being a part of our AngelList Syndicate. I’ll pull those out in a separate post, but if you’d like a preview you’ll find that on pages 11 – 17 below.